EXECUTIVE SUMMARY

|

Dear Fellow Investors,

Seeking to invalidate

Equity investing is usually approached as a search for the right stock(s). This mindset creates pressure to find opportunities and often leads to confirmation bias. Investors selectively focus on the positives, overlooking the negatives. An investor’s primary job, we have come to appreciate, should be not to select companies, but to try to reject them. Among roughly 2,000 listed companies in India seeing regular activity, perhaps around 100-200 are truly exceptional. The fastest way to find them is by systematically eliminating the ordinary ones.

Earlier, we researched companies hoping they would qualify for investment. Once time and effort had been invested, rejecting the idea felt like admitting failure. In reality, owning the wrong company is far more costly than abandoning research effort early. Today, when we encounter a potential investment, we first seek to invalidate the idea; look for reasons to reject it. Yes, this approach has the risk of rejecting a company that may turn around or perform well in the future. However, net-net, it saves the portfolio from sub-par companies, thereby lifting the overall quality of the portfolio and lowering risk (so long as we do not overpay).

Some of the key reasons we reject companies include:

- Difficult-to-understand businesses

- Businesses facing inevitable disruption

- Lack of durable competitive advantages

- Weak cash-flow generation or repeated capital raising

- Poor capital allocation or empire building

- Persistently low returns on capital, expected to continue in the future

- History of unfair treatment of minority shareholders

- Significant unexplained related-party transactions

- Complex holding structures and numerous subsidiaries

- High customer concentration

Notably, valuation is absent from this list. If a company survives our rejection process, it enters our study universe regardless of price. Great businesses often become attractive investments when temporary setbacks create opportunities.

Our goal is to adhere to this discipline every day, despite the psychological difficulty of doing so. The advantage is that we can focus our time and energy on understanding the best businesses within our circle of competence in greater depth, while gradually broadening that circle.

Time spent in sincerely rejecting a sub-par idea is time well spent.

A. PERFORMANCE

A1. Statutory PMS Performance Disclosure

| Year Ended | CED Long Term Focused Value (PMS) | BSE 500 TRI^ (Benchmark) | Difference | ||

|---|---|---|---|---|---|

| Return | Avg. Cash Eq. Bal. | Return | Trailing P/E | ||

| FY 2027 YTD | 12.4% | 17.9% | 12.1% | 23.7x | +0.3% |

| FY 2026 | 14.1% | 19.6% | -3.1% | 21.7x | +17.2% |

| FY 2025 | 10.3% | 21.0% | 6.0% | 23.4x | +4.3% |

| FY 2024 | 29.2% | 26.1% | 40.2% | 26.2x | -11.0% |

| FY 2023 | -4.3% | 30.0% | -0.9% | 22.3x | -3.4% |

| FY 2022 | 14.9% | 38.5% | 22.3% | 25.0x | -7.4% |

| FY 2021 | 48.5% | 29.0% | 78.6% | 38.0x | -30.1% |

| FY 2020* | -9.5% | 23.0% | -23.4% | 18.3x | +13.9% |

| Since Inception(7Y) | 15.4% | 26.6% | 15.2% | +0.2% | |

| ^TRI=Total Returns Index (includes dividends reinvested in addition to price movement); *From Jul 24, 2019; ‘Since inception’ performance is annualised; Note: As required by SEBI, the returns are calculated on time weighted average (NAV) basis. The returns are NET OF ALL EXPENSES AND FEES. The returns pertain to ENTIRE portfolio of our one and only strategy. Individual investor returns may vary from above owing to different investment dates. Annual returns are audited but not verified by SEBI. | |||||

Broad Indian market indices fell 10%-15% in March 2026 due to the US Iran war. We had changed our stance to aggressive and used the opportunity to add to our portfolio. As in the past, the markets recovered quickly, rising around 8%-10% back in the first 21 days of April where they remain currently. The next quarter’s earnings may remain volatile due to input cost inflation and supply chain issues from the lagging effects of Strait of Hormuz closure. That, along with the fact that there still remain some more reasonably priced pockets, may allow us to add more. Stance remains aggressive.

A2. Underlying business performance

| Past Twelve Months | Earnings per unit (EPU)2 | FY 2026 EPU (expected) |

|---|---|---|

| Mar 2026 | 12.51 | 11.8-12.83 |

| Dec 2025 (Previous Quarter) | 11.1 | |

| Mar 2025 (Previous Year) | 9.3 | |

| Annual Change | 34.4% | |

| CAGR since inception (Jun 2019) | 15.1% | |

| 1 Last four quarters ending Mar 2026. Results of Jun quarter are declared by Aug only. 2 EPU = Total normalised earnings accruing to the aggregate portfolio divided by units outstanding. 3 Please note: the forward earnings per unit (EPU) are conservative estimates of our expectation of future earnings of underlying companies. In past we have been wrong – often by wide margin – in our estimates and there is a risk that we are wrong about the forward EPU reported to you above. | ||

Earnings per unit – When you invest, you are allocated notional units and NAV. For Rs 50 lacs of investment you are allocated 50,000 notional units of NAV Rs 100. We track the earnings performance of our aggregate portfolio companies by dividing normalised earnings accruing to us (number of stocks held x earnings per share) by outstanding units.

Trailing Earnings: As against the guided range of Rs 10.8-11.2, the actual trailing earnings per unit for FY26 came in at Rs 12.5, 12% above our guidance and 34.4% above last year’s (including effects of cash equivalents that earn ~6%). This healthy growth was due to higher-than-expected earnings growth in four large holdings.

1-Yr Forward Earnings: We introduce FY27 forward earnings per unit guidance at Rs 11.8-12.8. This conservative guidance captures higher uncertainty after the US-Iran war as well as higher base of last year. We will revise the estimates after we study next quarter’s earnings.

A3. Underlying portfolio parameters

| Jun 2026 | Trailing P/E | Forward P/E | Portfolio RoIC | Portfolio Turnover1 |

|---|---|---|---|---|

| CED LTFV (PMS) | 22.2x | 21.1x-22.9x | 43.0%3 | 0% |

| BSE 500 | 23.7x2 | – | 18.5%2 | – |

| 1 ‘sale of equity shares other than liquid funds and client redemptions’ divided by ‘average portfolio value’ during the year to date period. 2Source: Asia Index. 3Portfolio Return on Invested Capital (RoIC) is on core equity positions. For BSE 500 index we share the RoE (Return on Equity) | ||||

Understanding the Numbers

Some of you have asked why we share the above tables and how to interpret these numbers. We share them to help you evaluate the performance largely through data, without having to rely on qualitative commentary.

Our belief is that if we buy good businesses and do not overpay, our long term returns should match or exceed the growth in earnings of the underlying companies. Over the last seven years, both portfolio earnings and NAV have compounded at roughly 15% per annum.

The first table shows annual and since-inception NAV returns. This disclosure is also required by regulation. Please note, the NAV returns are after around a quarter of the portfolio was in cash equivalents over the last 7 years.

The second table, which we consider more important, tracks the growth in earnings attributable to each unit of the portfolio. To account for inflows and outflows of capital, we use Earnings per Unit.

Like any metric, Earnings per Unit can be misleading if viewed in isolation. A portfolio manager could artificially boost this number by buying statistically cheap stocks with high current earnings, even if those businesses are in decline. Such companies may look attractive on today’s earnings but destroy value over time.

This is why Earnings per Unit should be viewed together with two other measures: long-term NAV returns and portfolio turnover.

If earnings per unit is growing, long-term NAV returns are healthy, and portfolio turnover remains low, it is a good indication that earnings growth is coming from owning improving businesses rather than from constantly trading between optically cheap stocks. These numbers since inception for us have been 15% NAV return, 15% earnings growth and 8% portfolio turnover annually.

The remaining metrics provide additional context. Portfolio Price-to-earnings (P/E) helps assess valuation discipline, while Returns on Equity (RoE) provides a measure of business quality. A reasonable P/E suggests we are not overpaying, and a high RoE indicates that the underlying businesses are strong and generating attractive returns on capital.

No single metric tells the full story. Taken together, however, these numbers provide a reasonably complete picture of what we own, how those businesses are performing, and whether our investment approach is working as intended.

B. DETAILS ON PERFORMANCE

B1. MISTAKES AND LEARNINGS

We did not discover any new mistakes this quarter.

B2. MAJOR PORTFOLIO CHANGES

Bought: We added to an existing position. It is now a major position. We have also introduced a new toehold 2% position. We will share more about it in future should it become a major position.

Sold: We did not sell any position this quarter.

B4. FLOWS AND SENTIMENTS

Artificial Intelligence (AI) & Foreign Flows

AI remains the dominant global investment theme and a major destination for capital flows. Unlike China, Taiwan, South Korea, or Japan, India has few direct beneficiaries of the AI infrastructure buildout. As a result, a portion of global capital has gravitated towards markets with exposure to semiconductors, AI hardware and related technologies.

There is also a concern that AI could disrupt parts of India’s services-led economy. Whether this ultimately proves true remains an open question, but it has contributed to a more cautious view on Indian equities, especially given their relatively full valuations.

Like every major technological revolution before it, AI has the potential to reshape industries and significantly improve productivity. The world is currently in the buildout phase, with enormous investments being made in chips, data centres, electricity, and other supporting infrastructure. History suggests that such periods are often accompanied by overbuilding. Railways, telecom networks and the internet all went through phases where infrastructure investment ran ahead of economic returns.

The ultimate winners may therefore not be the providers of infrastructure, but the applications built on top of it. During the internet era, the greatest value accrued not to owners of undersea cables but to businesses such as Amazon, Netflix and Meta that leveraged the network. Which AI applications will emerge as the long-term winners remains one of the most important unanswered questions for investors today.

Another possibility is that the current enthusiasm around AI eventually cools as infrastructure investments outrun near-term monetisation. If that happens, capital may rotate away from AI beneficiaries and towards markets such as India. Again, whether this plays out remains to be seen.

Retail Flows

While foreign investors have looked elsewhere, domestic retail investors continue to provide strong support to Indian markets. SIP inflows remain above Rs 30,000 crore per month and have become an important source of demand for equities.

However, there are early signs of moderation. The SIP stoppage ratio—the ratio of SIP accounts closed to new SIP accounts—crossed 100% in March and April 2026, indicating that more SIPs were closed than opened during those months. Lump-sum equity flows, which had remained positive for several months, turned negative in May with net outflows of around Rs 10,000 crore.

Domestic mutual funds have been the primary absorbers of shares sold by foreign investors, promoters, private equity funds and government (recently). In many ways, retail investors have acted as the anchor stabilising the market.

This is why retail flows remain one of the most important variables to track. If SIP inflows remain resilient, they can continue to support valuations and absorb supply. If they slow meaningfully, the impact is likely to be felt most in small-cap and mid-cap stocks, many of which continue to trade at premiums to their large-cap peers.

C. OTHER THOUGHTS

Convergence of Price and Value

Across markets and time, successful investing has rested on the principle of paying less for an asset than it is worth, or owning an asset whose price grows at least as much or faster than the growth in its worth.

The central challenge, therefore, is determining what an asset is actually worth.

The value/worth of any asset is the present value of the cash it will generate over its useful life. A piece of farmland, for example, derives its value from the net cash generated by the crops it produces after accounting for operating costs, capital investments and other expenses. The same principle applies whether one is valuing a farm, a bond, a rental property, or a business.

While the maths of valuation is simple, the difficulty lies in the fact that the calculation depends entirely on the future.

The magnitude, durability and variability of future cashflows can never be known with precision. Different investors looking at the same asset often arrive at very different conclusions. Markets exist to aggregate these differing views. Every day, participants reassess the future in light of new technologies, operating and economic data, government policies and geopolitical events. Human emotions, too, influence this process. Optimism encourages investors to extrapolate favourable outcomes further into the future. Pessimism does the opposite. Prices move as investors attempt to reflect their latest estimate of value based on these inputs.

History suggests that, over long periods, this messy process converges prices toward value. Over shorter periods, however, the divergence can be substantial. Importantly, “short term” in markets can mean several years.

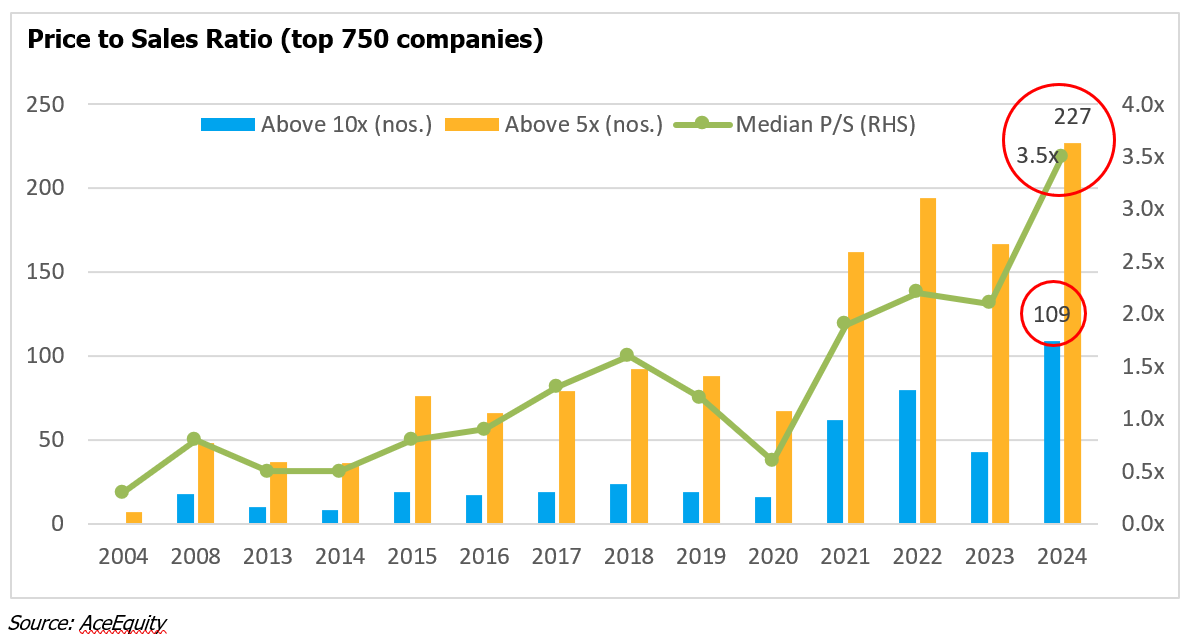

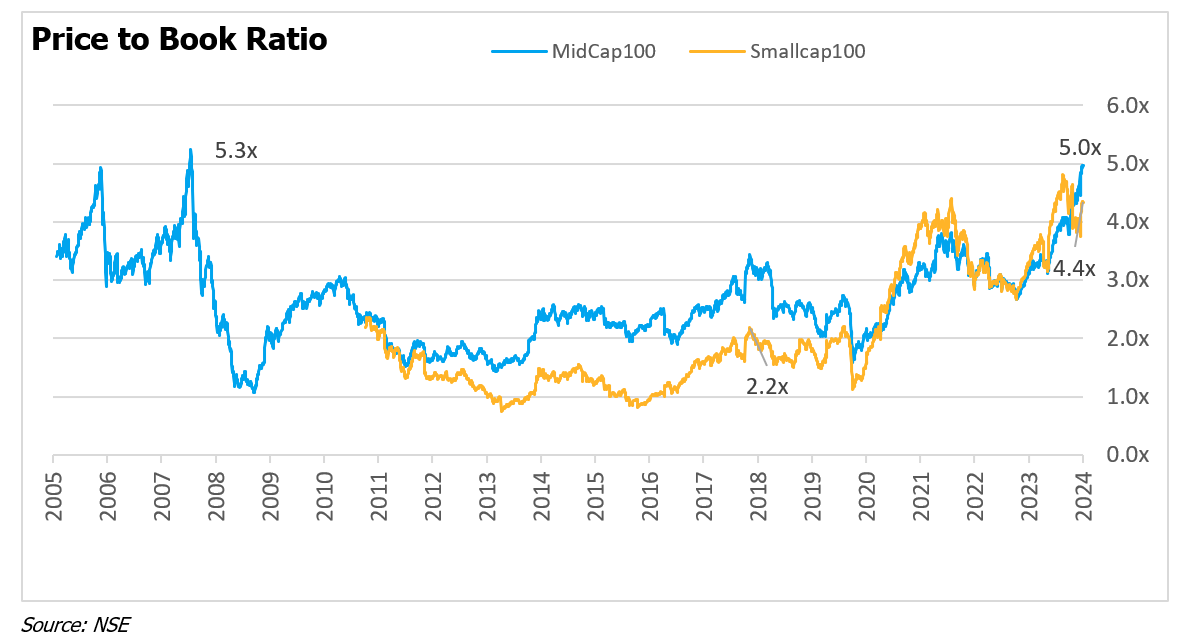

Recent developments have led some investors to question whether this relationship has weakened. Retail participation has increased dramatically. Mobile trading platforms have lowered barriers to entry, while social media, financial influencers and AI tools have made investing appear easier and more predictable. Investors have also become accustomed to policymakers stepping in during periods of market stress, strengthening the perception that meaningful declines will eventually be met with support. Reinforced by this rising tide, ‘Buy the Dip’ has become a widely accepted strategy. As a result, valuations have remained elevated for longer than many expected in several asset classes and market segments.

This naturally raises the question: has the market’s tendency to bring price and value together become weaker? Have assets reached a permanently higher plateau, echoing Irving Fisher’s famous observation shortly before the crash of 1929?

To be fair, some exceptional businesses do justify valuations that appear demanding. Investors often underestimate the longevity of companies with durable competitive advantages, causing their intrinsic value to compound faster than expected. Such businesses are rare. Value ultimately remains anchored to the cash generated.

Markets may assign a higher multiple to a rupee of earnings during optimistic periods, but they cannot manufacture earnings and cash flows.

Current enthusiasm for equities rests on the belief that they will continue to deliver attractive returns. History reminds us that this has not always been true, even over ten-year periods. Slower-than-expected earnings growth, higher interest rates, regulatory changes, shifts in leverage conditions or simply changing sentiment can alter the flow of capital. At the same time, higher prices encourage additional supply through promoter sales, private equity exits and secondary offerings.

The timing of convergence between price and value is impossible to predict. It can take far longer than expected and test the patience of disciplined investors. The principle, however, remains intact. Over time, cash flows and earnings exert a gravitational pull that markets struggle to escape indefinitely.

Price and value may travel separately for extended periods. Over time, they meet.

***

As always, gratitude for your trust and patience. Kindly do share your thoughts, if any. Your feedback helps us improve our services to you!

Kind regards

Sumit Sarda

Partner and Portfolio Manager

————————————————————————————————————————————————-

Disclaimer: Compound Everyday Capital Management LLP is SEBI registered Portfolio Manager with registration number INP 000006633. Past performance is not necessarily indicative of future results. All information provided herein is for informational purposes only and should not be deemed as a recommendation to buy or sell securities. This transmission is confidential and may not be redistributed without the express written consent of Compound Everyday Capital Management LLP and does not constitute an offer to sell or the solicitation of an offer to purchase any security or investment product. Reference to an index does not imply that the firm will achieve returns, volatility, or other results similar to the index.